If you have ever looked closely at a mutual fund account statement, you may have spotted a small code that starts with “ARN” — and wondered what it actually means. The ARN number in mutual fund investing is one of those behind-the-scenes details that quietly shapes who sells you a fund, who earns from it, and how the entire distribution system stays accountable.

ARN stands for AMFI Registration Number, and it is essentially the licence that lets a person or company legally distribute mutual funds in India. It matters to two very different groups: anyone hoping to build a career as a mutual fund distributor, and ordinary investors who simply want to understand what that code on their statement signifies. This guide covers both — what the ARN is, who issues it, how to get one in 2026, the latest fees and rules, the difference between ARN and EUIN, and why the ARN should matter to you even if you never plan to sell a single fund.

A quick note: this article is for educational and informational purposes only and is not investment advice. Processes and fees change over time, so verify current details on the official AMFI website before acting.

What Is an ARN Number in Mutual Fund?

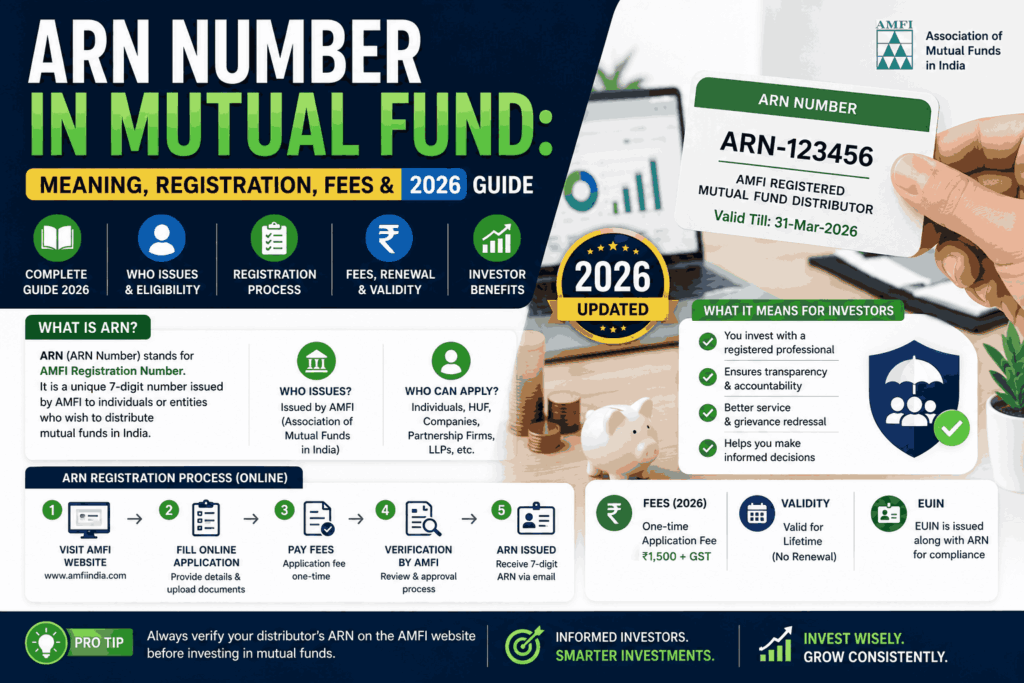

What is ARN in mutual fund terms? It is an identity code allotted by AMFI – the Association of Mutual Funds in India to all the authorised mutual fund distributors. Any individual financial advisor, bank, NBFC or online investment platform distributes mutual funds and takes commission from the same has to be registered under ARN. If it is not there, the distribution or sale of mutual fund scheme in India is not considered legal.

The ARN can be viewed as a sort of professional licence plate in the mutual fund realm. It’s known by all asset management companies (AMCs) in the country and the same ARN identifies a distributor across all of the country’s more than 40 fund houses, ranging from SBI Mutual Fund to HDFC, ICICI Prudential and more. Today, the mutual fund industry administers assets of well over ₹70 lakh crore and the ARN system plays an important role in keeping the vast, rapidly expanding industry transparent and accountable.

ARN Full Form and What It Looks Like

The ARN full form is AMFI Registration Number. A typical ARN is written as “ARN-” followed by a number — for example, ARN-123456. This code appears on the distributor’s AMFI-issued card and, importantly, on the statements of investors who invested through that distributor. It is how the system knows who sourced a particular investment and who is entitled to commission on it.

Who Issues the ARN, and Why It Exists

The ARN is issued by AMFI, the industry body which regulates ARN in mutual funds, under the overall aegis of Securities and Exchange Board of India (SEBI). SEBI and AMFI established the guidelines of selling mutual funds and the concept had a sole objective – investor’s money.

There are three practical reasons for the existence of the ARN. First, accountability – each and every regular-plan transaction can be followed back to a registered distributor. Secondly, competence — to get the ARN, the distributor has to pass an exam that defines his competence, so they have to prove that they know the products and the rules. Third, trust — investors can check whether the person advising them is registered or not, or if they are some fly-by-night who hasn’t been qualified to give financial advice. The ARN is a positive measure to protect against mis-selling in this market.

Who Needs an ARN Number in Mutual Fund Distribution?

An ARN is required by anyone who wants to distribute mutual funds and be paid for it, including:

- Individual distributors and IFAs (independent financial advisors) who sell funds directly to clients.

- Banks, NBFCs and corporate distributors that offer mutual funds alongside other products.

- Online platforms and fintech apps that distribute regular-plan mutual funds.

- Post offices, societies, trusts and partnership firms that participate in distribution.

Who does not need an ARN? Ordinary investors don’t — you never need an ARN to buy funds for yourself. And fee-only advisers who charge clients directly operate under a separate SEBI registration (more on that distinction later). The ARN is specifically the badge of the commission-earning distributor.

ARN vs EUIN: What’s the Difference?

If you have a corporate distributor or a bank, you will often see two codes on a transaction — an ARN and an EUIN. They are related but do different jobs:

| Aspect | ARN | EUIN |

| Full form | AMFI Registration Number | Employee Unique Identification Number |

| Who it identifies | The distributor (individual or entity) | The specific employee who advised the deal |

| Main purpose | Authorises distribution & commission | Fixes accountability for the advice given |

| Who needs it | Every mutual fund distributor | Employees/sales staff of (mainly non-individual) distributors |

| How it’s linked | Stands on its own | Always linked to a distributor’s ARN |

| Validity | 3 years | 3 years |

The EUIN matters most for investor protection. If a relationship manager at a bank advises you to buy a fund, the EUIN records exactly who that person was — so if a complaint of mis-selling arises later, the advice can be traced to an individual, not just a faceless institution. On transaction forms, if the EUIN is left blank, you are usually asked to confirm the deal was “execution-only,” meaning no advice was given.

Eligibility to Get an ARN Number

AMFI and SEBI set clear eligibility conditions before anyone can be allotted an ARN:

- Pass the NISM exam. Individuals must clear the NISM Series V-A: Mutual Fund Distributors Certification Examination, conducted by the National Institute of Securities Markets.

- Senior-citizen route via CPE. Individuals aged 50 or above (with the required years of relevant experience, certified by an AMC) may qualify through a Continuing Professional Education (CPE) programme instead of the full NISM exam.

- Agree to the Code of Conduct. All applicants must commit to AMFI’s code of conduct and the undertakings in the application form.

- Corporate eligibility. Companies, banks, LLPs and similar entities apply as non-individual distributors, with their certified employees obtaining EUINs.

How to Apply for an ARN Number in Mutual Fund (2026 Process)

As of 2026, ARN registration is fully online and paperless. Following an AMFI notice in September 2024, the old physical biometric step was discontinued and replaced with Aadhaar-based online verification — making registration faster and far simpler. Here is how it works:

- Clear the NISM Series V-A exam (or complete the CPE route if you qualify as a senior citizen).

- Register on the AMFI online portal (operated through CAMS) and choose ARN as your application type and the correct category (individual or corporate).

- Enter your details — name as per PAN, date of birth, NISM certificate details, bank account and address — and upload the required documents.

- Complete the KYD (Know Your Distributor) step using Aadhaar-based online verification via OTP. No fingerprint or branch visit is needed.

- Pay the fee online through UPI, debit/credit card or net banking.

- Receive your ARN, typically within about T+3 business days, with a soft copy of the ARN card sent to your registered email.

Documents You’ll Typically Need

Keep these ready to avoid delays: your PAN, Aadhaar (for KYD), your NISM or CPE certificate, bank account details, address proof and a passport-size photograph. For corporate applicants, additional entity documents and authorised-signatory details apply.

ARN Registration and Renewal Fees (2026)

AMFI reduced distributor fees significantly a few years ago to widen participation, and the current structure remains modest for individuals. The figures below are indicative — always confirm the latest amounts in AMFI’s official fee structure, since they can be revised.

| Category | Registration fee | Renewal fee |

| Individuals & proprietorship firms | ~₹1,500 | ~₹750 |

| EUIN (employees) | ~₹500 | ~₹750 |

| Banks, societies, trusts, HUFs, partnerships | ~₹10,000 | ~₹5,000 |

| OPC, LLPs, private limited companies | ~₹20,000 | ~₹10,000 |

All fees are subject to applicable GST. Renewal fees are generally around half the registration fee. Verify current rates on the AMFI website before paying.

ARN Validity and Renewal

An ARN is valid for three years from the date of issue. To keep distributing without interruption, you must renew it online before it expires, and renewal requires your certification to be current — either a valid NISM certificate or the prescribed CPE refresher. The renewal itself mirrors the online application: log in to the AMFI portal, update details if needed, and pay the renewal fee.

Letting an ARN lapse has real consequences. Once expired, a distributor cannot solicit fresh investments or earn new commission on transactions until the ARN is renewed and reactivated. For a working distributor, allowing a lapse can mean a genuine break in income, so renewal dates are worth tracking carefully.

Why the ARN Number Matters to Investors (Not Just Distributors)

Even if you never plan to distribute funds, the ARN is worth understanding, because it directly affects your money:

- It shows who earns from your investment. If you bought a regular plan through a distributor, their ARN appears on your statement and Consolidated Account Statement (CAS) — and that distributor earns ongoing trail commission, funded from the fund’s expense ratio.

- It separates regular from direct. A direct plan has no ARN because there is no distributor in between. That’s why direct plans carry a lower expense ratio and tend to deliver slightly higher returns over the long run.

- It lets you verify credibility. Before trusting someone with your investments, you can confirm their ARN is genuine and active — a simple but powerful fraud check.

- It gives you control. You can change the distributor attached to your folio, or move to a direct plan, if you no longer value the service you’re paying for.

How to Check or Verify an ARN Number

AMFI has a public database of all registered funds distributors on its website, which serves as the official ARN locator for investors. You may search by the ARN number to check if the registration is valid and active or you can search by the distributor’s name to check if the registration is valid and active. This takes one minute, and it’s the best method to ensure that the individual who’s guiding your money is in fact authorised.

ARN Distributor vs SEBI Registered Investment Adviser (RIA)

This is the distinction most investors miss — and it matters for the kind of advice you actually receive. An ARN holder is a distributor, not necessarily an independent adviser. The two operate under different registrations, earn money in different ways, and owe you different duties.

| Aspect | MF Distributor (ARN) | Investment Adviser (RIA) |

| Registered with | AMFI (holds an ARN) | SEBI (holds an RIA licence) |

| Earns from | Commission/trail paid by AMCs | A fee paid directly by you |

| Plan you get | Regular plan | Can advise on direct plans |

| Core role | Distribute & execute; incidental advice | Personalised, fiduciary advice |

| Cost to you | Built into the fund’s expense ratio | An explicit, agreed advisory fee |

| Certification | NISM Series V-A | NISM Series X-A & X-B plus qualifications |

Neither model is automatically “better” — a good distributor can add real value through hand-holding and last-mile access, especially for first-time investors, while an RIA suits those who want conflict-free, fee-based advice. The key is simply to know which one you’re dealing with, so you understand how they’re paid and what you can expect from them.

Regular Plans vs Direct Plans: The ARN Connection

Every mutual fund scheme comes in two variants, and the ARN sits right at the heart of the difference. A regular plan is bought through an ARN-holding distributor, who earns trail commission funded from the scheme’s expense ratio. A direct plan is bought straight from the AMC with no distributor in between — so there is no commission, and the expense ratio is lower.

That gap looks small on paper but compounds powerfully over time. A direct plan often costs roughly 0.5% to 1% less per year than its regular twin. On a long-running SIP held for 15 to 20 years, that seemingly tiny annual difference can quietly add up to a substantial amount, purely because less is shaved off your returns each year.

So which should you pick? It comes down to what you actually value:

- A regular plan (with an ARN distributor) makes sense if you genuinely benefit from guidance, paperwork help and someone to keep you invested during market scares — that service has real worth, especially for first-time investors.

- A direct plan suits you if you’re confident making your own decisions, or you already pay a SEBI-registered adviser separately and simply want the lowest-cost way to hold the funds.

There’s no universally correct answer — just be clear about what you’re paying for. The simple tell is on your statement: if you see an ARN, you’re in a regular plan and a distributor is earning from it; if that code is absent, you’re already in direct.

Pros and Cons of the ARN System

Pros

- Ensures distributors are certified, vetted and accountable — a real layer of investor protection.

- Gives distributors a single, portable identity recognised across every AMC in India.

- Improves transparency — investors can see and verify who sourced their investment.

- Extends mutual fund access to small towns and first-time investors through a wide distributor network.

- Offers a low-cost, accessible career path, especially after AMFI cut registration fees.

Cons

- Regular plans funded via ARN commission carry higher expense ratios than direct plans.

- Commission structures can create an incentive to push higher-paying products — the mis-selling risk the EUIN tries to curb.

- An ARN proves a distributor is certified, not that they are a conflict-free, expert adviser.

- Distributors face ongoing renewal and compliance obligations every three years.

Latest 2026 Updates on the ARN Process

The biggest recent shift is how much simpler registration has become. Following AMFI’s September 2024 notice, the ARN and EUIN process moved fully online: physical biometric verification was discontinued, Aadhaar-based online KYD became standard, and approvals now typically come through within about three business days, with digital cards delivered by email. For aspiring distributors, the barrier to entry has rarely been lower.

Alongside this, AMFI’s reduced fee structure continues to encourage new and younger distributors, particularly in Tier-2 and Tier-3 cities, as the industry pushes deeper into under-served markets. With mutual fund assets now well past ₹70 lakh crore and SEBI maintaining its focus on commission transparency, EUIN-based accountability and curbing mis-selling, the ARN framework remains central to keeping India’s mutual fund boom both accessible and trustworthy. As always, confirm the most current rules and fees directly with AMFI, since the regulator and the industry body periodically refine the process.

Frequently Asked Questions

What is an ARN number in mutual fund investing?

ARN stands for AMFI Registration Number — a unique code issued by the Association of Mutual Funds in India (AMFI) to mutual fund distributors, agents and intermediaries authorised to sell mutual funds and earn commission. A typical ARN looks like ARN-123456 and identifies who sourced an investor’s investment.

Is an ARN mandatory to sell mutual funds in India?

Yes. No individual or entity can legally distribute or sell mutual fund schemes in India, or earn commission for doing so, without a valid ARN issued by AMFI. It is a regulatory requirement backed by SEBI and AMFI guidelines.

Do investors need an ARN number?

No. Investors never need an ARN — it is only for distributors. If you invest through a distributor (a regular plan), their ARN appears on your statement; if you invest in a direct plan, there is no ARN because no distributor is involved.

What are the ARN registration and renewal fees in 2026?

For individuals and proprietorship firms, registration is around ₹1,500 and renewal around ₹750, plus GST. Corporate categories pay more (roughly ₹10,000 to ₹20,000 to register). EUIN registration is around ₹500. Always check the latest fee structure on the AMFI website, as fees can change.

How long is an ARN valid, and how is it renewed?

An ARN is valid for three years from the date of issue. It must be renewed online before expiry, which requires keeping your NISM certification current (or completing the prescribed CPE). If it lapses, you cannot transact or earn fresh commission until it is renewed.

What is the difference between ARN and EUIN?

The ARN identifies the distributor (the individual or company), while the EUIN identifies the specific employee or salesperson who advised on a transaction. The EUIN is linked to the ARN and exists to fix accountability for the advice given, which helps curb mis-selling.

How can I check if a mutual fund distributor’s ARN is valid?

You can verify an ARN on the AMFI website, which maintains a public directory of registered mutual fund distributors. Search by the ARN number or the distributor’s name to confirm the registration is valid and active before investing through them.

Final Verdict: Why the ARN Number in Mutual Fund Investing Matters

The ARN number in mutual fund investing is far more than a string of digits on a statement. For distributors, it is the essential licence — the proof of certification that lets them legally build a career helping others invest. For investors, it is a quiet but powerful transparency tool: it tells you who is earning from your money, helps you separate regular plans from cheaper direct plans, and lets you verify that the person guiding you is genuinely authorised.

If you’re planning to become a distributor, the 2026 online process makes getting your ARN quicker and cheaper than ever — clear the NISM exam, register on the AMFI portal, complete the Aadhaar-based KYD, and you can be up and running within days. And if you’re an investor, take a moment to look up the ARN on your statement, understand whether you’re in a regular or direct plan, and know the difference between a distributor and a fee-only adviser. That small bit of awareness can save you money and help you invest with genuine confidence.