Most people in India want to save money regularly — but between rent, EMIs, school fees, and daily expenses, saving a lump sum at the end of the month often feels impossible. A Recurring Deposit solves that problem by turning discipline into a product.

You commit to depositing a fixed amount every month — say Rs. 2,000 or Rs. 10,000 — and the bank pays you interest on the growing pool of money until your chosen term ends. At maturity, you receive everything back: your principal deposits plus compounded interest. No market risk, no complexity, and no missed EMI anxiety.

This guide goes well beyond surface definitions. It covers how recurring deposit interest is actually calculated, what banks are offering in mid-2026, how RD income is taxed, when breaking one early makes sense, and how it stacks up against Fixed Deposits and mutual fund SIPs — so you can decide whether an RD belongs in your savings plan.

| Quick Snapshot — Recurring Deposit Minimum deposit: Rs. 100/month (most banks) Typical tenure: 6 months to 10 years Interest compounding: Quarterly (most banks) Interest rate range (2026): 5.50% – 8.05% p.a. Tax on interest: Added to income, TDS applies if interest > Rs. 40,000/year Risk: Zero (guaranteed by bank / DICGC up to Rs. 5 lakh) |

What Is a Recurring Deposit? A Plain-English Explanation

The recurring deposit meaning is straightforward: It is a term deposit that the banks, post office, and select NBFCs offer in India, where you are fixed to deposit a certain amount at regular intervals, usually every month, over a specified term. The bank pays back the amount of money you invested in an account and the interest you have earned until you reach the end of your term.

It is like a stack of Fixed Deposit accounts. The mini-FD account is created as you make your monthly payments into an RD account. Both mini-FDs will get interest from the day of the deposit till maturity. Each deposit collects interest over the same period of time, but for a different amount of time because they were made at different times, and all of them are due to be collected on the same day. The bank determines the interest for each instalment and adds them together. After understanding the basic concept of recurring deposit, you will find it easy to understand the interest calculation, tax treatment and comparison with other savings options.

The money in an RD is reserved (with some provisions for closing the account early), which helps keep the savings habit intact, rather than spending the extra money in a regular savings account.

Key Characteristics of a Recurring Deposit

| Feature | Typical Terms |

| Minimum Monthly Instalment | Rs. 100 (most public sector banks), Rs. 500–1,000 (private banks) |

| Maximum Monthly Instalment | No upper limit for most banks |

| Minimum Tenure | 6 months |

| Maximum Tenure | 10 years (some banks offer up to 20 years via post office) |

| Interest Compounding | Quarterly (standard for Indian banks per RBI norms) |

| Premature Closure | Allowed with penalty (usually 0.5%–1% rate reduction) |

| Partial Withdrawal | Not allowed (differs from savings account) |

| Nomination Facility | Available |

| Auto-Renewal | Available at many banks |

| Loan Against RD | Up to 80%–90% of deposit value (varies by bank) |

How a Recurring Deposit Works — Step by Step

Understanding the mechanics makes you a better saver. Here is the lifecycle of a typical RD account:

Step 1 — Opening the Account

You choose a monthly instalment amount (e.g., Rs. 5,000), a tenure (e.g., 2 years = 24 months), and a bank. The bank quotes you an interest rate — say 7.00% per annum. You then provide standing instructions for auto-debit from your savings account on the same date each month.

Step 2 — Monthly Deposits

On your chosen date each month, the fixed instalment is debited from your linked savings account and credited to your RD account. Missing a payment attracts a penalty — typically Rs. 1 to Rs. 1.50 per Rs. 100 per month of delay. Multiple missed payments can lead to the RD account being classified as irregular.

Step 3 — Interest Accrual

Each monthly instalment earns interest from the day it is deposited. Interest accrues on a quarterly compounding basis for most Indian banks, as mandated by the Reserve Bank of India (RBI). This means every instalment’s interest is compounded four times a year.

Step 4 — Maturity

At the end of the tenure, the bank credits the full maturity amount — your total principal (number of months x monthly instalment) plus all accumulated interest — to your linked savings account. You receive a maturity receipt which you can use for tax purposes.

The RD Interest Calculation Formula

The standard formula banks use to calculate RD maturity value is:

M = R × [(1 + i)^n – 1] / [1 – (1 + i)^(–1/3)]

Where: M = Maturity Value | R = Monthly Instalment | i = Rate of Interest / 400 (quarterly compounding) | n = Number of Quarters

This formula looks intimidating but most banks provide an online RD calculator on their website. Enter your monthly amount, tenure, and rate — the maturity value appears instantly. Always use the bank’s own calculator for exact figures, since minor rounding differences exist between institutions.

Worked Example — Rs. 5,000/month for 2 Years at 7.00% p.a.

| Parameter | Value |

| Monthly Instalment | Rs. 5,000 |

| Tenure | 24 months (8 quarters) |

| Interest Rate | 7.00% p.a. (quarterly compounding) |

| Total Amount Deposited | Rs. 1,20,000 |

| Approximate Maturity Value | Rs. 1,28,755 |

| Total Interest Earned | Rs. 8,755 |

| Effective Yield | ~7.12% (slightly above stated rate due to quarterly compounding) |

Notice the effective yield is slightly higher than the stated rate — that is the compounding effect working in your favour, even on a modest sum.

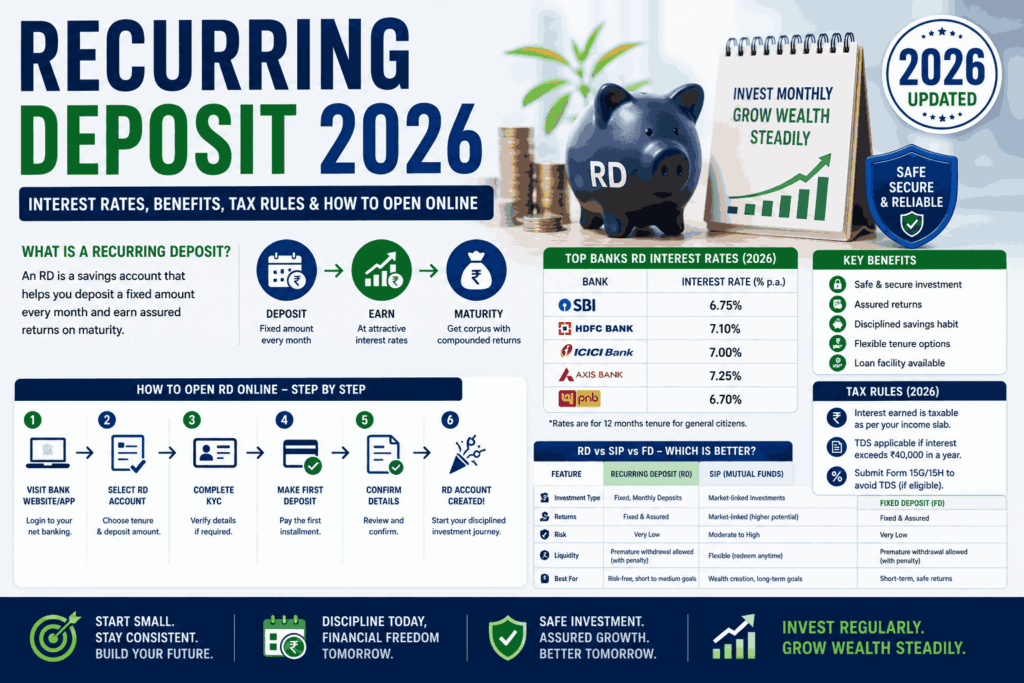

Recurring Deposit Interest Rates in India — Mid-2026 Comparison

Interest rates on recurring deposits closely track Fixed Deposit rates at the same bank. Most banks apply the same rate to RDs as they do to FDs of equivalent tenure. After the RBI held the repo rate and then made calibrated cuts through 2025–2026, RD rates have stabilised in the 6.50%–8.05% range depending on the bank and tenure.

Senior citizens (age 60 and above) typically receive an additional 0.25% to 0.75% over the regular rate — a significant benefit worth factoring in if you are planning retirement savings.

Indicative RD Interest Rates — Major Indian Banks (Mid-2026)

| Bank | General (1-2 Yr) | Senior Citizen | Min. Monthly Deposit |

| State Bank of India (SBI) | 6.80% | 7.30% | Rs. 100 |

| HDFC Bank | 7.00% | 7.50% | Rs. 1,000 |

| ICICI Bank | 7.00% | 7.50% | Rs. 500 |

| Bank of Baroda | 6.85% | 7.35% | Rs. 100 |

| Punjab National Bank | 6.80% | 7.30% | Rs. 100 |

| Axis Bank | 7.10% | 7.85% | Rs. 500 |

| Kotak Mahindra Bank | 7.20% | 7.70% | Rs. 500 |

| IDFC First Bank | 7.50% | 8.00% | Rs. 500 |

| AU Small Finance Bank | 7.75% | 8.25% | Rs. 500 |

| Utkarsh SFB | 8.00% | 8.50% | Rs. 500 |

| Post Office RD (India Post) | 6.70% | 6.70%* | Rs. 100 |

*Post Office RD does not offer a senior citizen rate differential. Rates are indicative and subject to change. Always verify the current rate with your bank or post office before opening an account.

Small Finance Banks (SFBs) like AU, Utkarsh, and Suryoday consistently offer higher rates than large commercial banks, reflecting their higher cost of funds. These banks are regulated by the RBI, and deposits up to Rs. 5 lakh are covered by DICGC insurance — making them a legitimate option for rate-conscious savers.

Types of Recurring Deposit Accounts in India

Recurring Deposits are not one-size-fits-all. Banks have designed several variants to serve different customer segments:

Regular RD

The standard product most people think of when they hear ‘Recurring Deposit’. Fixed monthly instalment, fixed tenure, fixed rate locked at the time of opening. The rate does not change even if the bank revises its rate card during your tenure.

Flexi RD (Variable Amount RD)

A more recent innovation offered by banks like SBI (MODS), HDFC, and ICICI. You commit to a core monthly deposit but can increase it in multiples (e.g., Rs. 500 steps) in months when you have a surplus. Interest is calculated separately on each instalment amount. This suits professionals with variable income, freelancers, or salaried individuals who receive performance bonuses.

Senior Citizen RD

Structurally identical to a regular RD but with an enhanced interest rate (0.25%–0.75% higher) for customers aged 60 and above. The benefit applies throughout the tenure — you do not need to re-register each year. Some banks extend this benefit to individuals aged 55 and above under certain schemes.

Minor RD / Children’s RD

Opened in the name of a minor (below 18 years), with the parent or legal guardian operating the account. A powerful tool for systematically building a child’s education or higher-study fund. On attaining majority, the minor can operate the account independently after KYC update.

NRE / NRO Recurring Deposit

In simple terms, nre recurring deposit meaning is that Non-Resident Indians (NRIs) may open RD accounts in India and the interest as well as the principal will be freely repatriable — and importantly, the interest earned on the NRE accounts will be exempt from tax in India. NRO RD in contrast, is being opened for income earned in India (rent, pension etc.) and is taxable.

Post Office Recurring Deposit

Operated by India Post under the National Savings Schemes umbrella, the Post Office RD has a fixed tenure of 5 years and a current rate of 6.70% p.a. (compounded quarterly). Deposits as low as Rs. 100 per month are accepted, making it the most accessible product for rural and semi-urban savers. The government backing makes it one of the safest savings instruments available.

| RD Type | Best For | Unique Feature |

| Regular RD | Salaried employees, first-time savers | Rate locked at opening — predictable |

| Flexi RD | Freelancers, variable income earners | Top-up deposits allowed |

| Senior Citizen RD | Retirees (60+) | Higher interest rate |

| Minor RD | Parents saving for children | Can be converted on majority |

| NRE RD | NRIs with foreign income | Tax-free interest, fully repatriable |

| Post Office RD | Rural/low-income savers | Government-backed, Rs. 100 minimum |

Recurring Deposit — Advantages and Disadvantages

Advantages

- Guaranteed returns: Unlike stocks or mutual funds, RD returns are fixed and guaranteed. You know exactly how much you will receive at maturity — no surprises.

- Habit of forced savings: The auto-debit mechanism removes the temptation to spend. Many people save more through an RD than through a free savings account.

- Low entry barrier: You can start with as little as Rs. 100 per month at SBI and India Post — genuinely accessible even on modest incomes.

- Flexible tenure: From 6 months to 10 years, you can match the RD tenure to your specific financial goal — a vacation fund, emergency cushion, or children’s fees.

- DICGC insurance: Deposits in banks are insured up to Rs. 5 lakh per depositor per bank under the Deposit Insurance and Credit Guarantee Corporation scheme. Your capital is protected.

- Loan against RD: Most banks allow you to borrow up to 80%–90% of your RD balance as an overdraft facility. This means you do not need to break the RD in a financial emergency — you can borrow against it.

- Senior citizen benefit: The additional interest rate for senior citizens (0.25%–0.75%) meaningfully boosts post-retirement savings income.

- No market risk: Your returns are not affected by stock market crashes, inflation spikes in commodity markets, or currency volatility. This peace of mind has tangible value.

Disadvantages

- Lower returns than equity: Over a 5-10 year horizon, diversified equity mutual funds have historically outperformed RD returns by a significant margin. For long-term wealth creation, RDs alone are insufficient.

- Taxable interest: RD interest is added to your annual income and taxed at your applicable income tax slab. For someone in the 30% tax bracket, the post-tax return on a 7% RD is only ~4.9% — which may not beat inflation.

- TDS deduction: Banks deduct 10% TDS if your total interest income from deposits exceeds Rs. 40,000 per year (Rs. 50,000 for seniors). This is recoverable at ITR filing if your income is below the taxable limit, but requires paperwork.

- Penalty for missed payments: Forgetting to maintain a sufficient balance in your linked savings account leads to missed RD debits, which attract penalty fees and can complicate your account status.

- No partial withdrawals: Unlike a savings account, you cannot withdraw Rs. 5,000 from an RD mid-tenure. You either keep all of it or close the entire RD (with early closure penalty).

- Premature closure penalty: Closing an RD before the original tenure ends typically results in a 0.5%–1.0% interest rate reduction on the applicable rate, meaning you earn less than the promised rate.

- Fixed monthly commitment: If your income drops unexpectedly (job loss, medical emergency), the monthly RD commitment becomes a burden. Flexi RD variants help but are not universally available.

Tax on Recurring Deposit Interest — What You Need to Know in 2026

Recurring Deposit interest is one of those areas where many first-time investors make a costly mistake — they do not account for tax while comparing returns. Here is how RD taxation works:

How RD Interest Is Taxed

Interest earned on a RD is classified as ‘Income from Other Sources’ under the Income Tax Act, 1961. It is added to your gross total income and taxed at your applicable slab rate — 5%, 20%, or 30% depending on your income level under the new tax regime.

This is fundamentally different from ELSS funds or PPF, where returns enjoy special tax treatment. There is no separate exemption for RD interest under any current provision.

TDS on Recurring Deposits

Banks deduct Tax Deducted at Source (TDS) at 10% if your total interest from deposits (across all accounts at that bank) exceeds Rs. 40,000 in a financial year (Rs. 50,000 for senior citizens — enhanced from Rs. 40,000 as per Budget 2025–26). This TDS is on your behalf and is adjustable against your final tax liability when you file your ITR.

If you are in the nil-tax bracket (income below Rs. 3 lakh under new regime / Rs. 2.5 lakh under old regime), you can submit Form 15G (for non-seniors) or Form 15H (for seniors) to your bank at the start of each financial year to request that no TDS be deducted. This avoids the refund-chasing process.

When Does TDS Apply on RD?

| Category | TDS Threshold | TDS Rate | Form to Avoid TDS |

| General depositor (below 60) | Rs. 40,000/year | 10% | Form 15G |

| Senior citizen (60–80 years) | Rs. 50,000/year | 10% | Form 15H |

| Super senior citizen (80+) | Rs. 50,000/year | 10% | Form 15H |

| NRI (NRO account) | All interest | 30% | Not applicable |

| NRI (NRE account) | Tax-exempt | Nil | Not required |

| Tax Planning Tip If you are distributing Rs. 10,000/month across two or three different banks’ RD accounts, each bank’s interest may stay below the TDS threshold individually — so no TDS is deducted at any single bank. You still owe tax on the combined interest when filing your ITR, but you avoid the TDS process. This is legal tax planning, not evasion — but consult a CA if your situation is complex. |

Recurring Deposit vs Fixed Deposit vs SIP — A Practical Comparison

Three savings/investment instruments dominate the conversation for moderate-risk Indian savers. Understanding where each one belongs in your financial plan is more useful than declaring one ‘the best’.

| Parameter | Recurring Deposit (RD) | Fixed Deposit (FD) | SIP (Mutual Fund) |

| Investment Style | Monthly, small fixed amounts | One-time lump sum | Monthly, any amount |

| Returns | Fixed (6.5%–8% p.a.) | Fixed (6.5%–8% p.a.) | Market-linked (10–15% historical avg) |

| Risk Level | Zero (guaranteed) | Zero (guaranteed) | Low to High (market risk) |

| Liquidity | Low (locked until maturity) | Low (locked until maturity) | High (can redeem anytime for open-ended) |

| Minimum Amount | Rs. 100/month | Rs. 1,000 (most banks) | Rs. 100–500/month (most funds) |

| Tax on Returns | Slab rate (income) | Slab rate (income) | LTCG 12.5% above Rs. 1.25 lakh / STCG 20% |

| Best Tenure | 6 months – 5 years | 7 days – 10 years | 5 years+ for equity |

| DICGC Protection | Yes (up to Rs. 5 lakh) | Yes (up to Rs. 5 lakh) | No (SEBI regulated, not insured) |

| Penalty for Early Exit | Yes (0.5%–1% rate cut) | Yes (0.5%–1% rate cut) | Exit load (1% if redeemed < 1 year, most funds) |

| Inflation Beating Potential | Marginal (at best) | Marginal (at best) | Yes (historically, over long term) |

| Loan Against Investment | Yes (80%–90%) | Yes (80%–90%) | Yes (varies by AMC) |

| Suitable For | Goal-based short saving | One-time surplus parking | Long-term wealth creation |

Expert View: When Should You Choose RD Over SIP?

An RD makes more sense than a SIP when: your goal is less than 3 years away (short-term goals do not benefit from equity market cycles); you have zero risk tolerance (e.g., saving for a child’s school fee that is due next year); you are building an emergency fund and want guaranteed access to a known amount; or you are a first-time saver who needs the psychological anchor of a fixed monthly commitment with a guaranteed outcome.

A SIP makes more sense when: your goal is 7+ years away; you want your savings to compound at a rate that outpaces inflation over the long term; and you are comfortable tolerating interim portfolio fluctuations for potentially higher gains.

For most people, a combination works best — RD for short-term goals and emergency funds, SIP for long-term wealth building.

Premature Closure of Recurring Deposit — Rules and Impact

Life is unpredictable. If you need to close your RD before the maturity date, here is what to expect:

How Premature Closure Works

Most banks allow premature closure of an RD account at any time after a minimum holding period (often 3 months at most banks, 1 month at a few). The process involves visiting the branch or using net banking / mobile app to submit a premature closure request.

The interest paid on premature closure is calculated at the rate applicable to the tenure actually completed — not the original booked rate — and a penalty of 0.50% to 1.00% is deducted from that applicable rate.

Premature Closure Penalty — Example

| Scenario | Detail |

| Original tenure booked | 24 months at 7.00% p.a. |

| Actual holding period | 10 months |

| Rate for 10-month FD (bank’s current card rate) | 6.50% p.a. |

| Penalty applied | 1.00% |

| Effective interest rate paid | 5.50% p.a. |

| Your loss vs original plan | ~1.50% p.a. on 10 months of deposits |

The actual penalty amount in rupees depends on your deposit amount and tenure. Many banks have an online premature withdrawal calculator — use it before closing to understand the exact impact.

When Breaking an RD Early Is the Smart Move

- If you receive a lump sum (bonus, inheritance) and want to reinvest in a higher-rate instrument — the gain from the new investment may offset the premature closure penalty.

- If RD rates have dropped significantly since you opened and you want to park money in a better-yielding alternative.

- If you need the funds for a genuine emergency and no loan-against-RD facility is available or suitable.

In most other cases, availing a loan against the RD (up to 80–90% of balance) is preferable to premature closure — you keep the RD earning interest while meeting your short-term need.

How to Open a Recurring Deposit Account in 2026

Opening a RD Account is faster than ever in 2026. Most major banks allow end-to-end online account opening in under 5 minutes for existing customers.

Method 1: Online (Net Banking / Mobile App) — For Existing Bank Customers

- Log in to your bank’s net banking portal or mobile app.

- Navigate to ‘Deposits’ or ‘Open New Account’ > ‘Recurring Deposit’.

- Enter the monthly instalment amount, select tenure, and verify the applicable interest rate.

- Link the RD to your savings account for auto-debit.

- Confirm with OTP sent to your registered mobile.

- Your RD account number is generated instantly. The first instalment is debited from your savings account on the next scheduled date.

Method 2: Branch Walk-In — For New Customers or Non-Digital Users

- Visit your nearest bank branch with: Aadhaar card, PAN card, one passport-size photograph.

- Fill out the RD opening form (available at the counter).

- Submit KYC documents if you are a new customer.

- Provide a cheque or direct debit mandate for the monthly instalment.

- You receive an RD passbook or a paper certificate as confirmation.

Method 3: Post Office RD — For Rural and Low-Income Savers

- Visit any Head Post Office or Sub-Post Office.

- Fill out Form-1 (available free at the counter).

- Submit Aadhaar and PAN (or valid alternative ID documents).

- Deposit the first month’s instalment in cash or cheque.

- Deposits from Month 2 onwards can be made at any post office branch.

| 2026 Update — Video KYC (V-KYC) Many banks including SBI, HDFC, ICICI, and Axis now allow Video KYC for new customers who want to open an RD without visiting a branch. After filling out the online form, a brief video call with a bank representative verifies your identity. Your RD is opened within 24 hours. This has dramatically reduced friction for first-time bank customers in Tier 2 and Tier 3 cities. |

Is Your Recurring Deposit Safe? Regulation and Deposit Insurance

A common question, especially after a few cooperative bank failures in recent years, is whether recurring deposits are truly safe. The answer is nuanced but broadly reassuring.

DICGC Coverage

The Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India, insures all bank deposits — including recurring deposits — up to Rs. 5 lakh per depositor per bank. This limit covers all your deposits at a single bank in aggregate (savings + FD + RD), not per account.

If you have Rs. 3 lakh in an FD and Rs. 3 lakh in an RD at the same bank, your combined insured limit is still Rs. 5 lakh — not Rs. 10 lakh. To maximise insurance coverage, spread deposits across multiple banks if your total exceeds Rs. 5 lakh at any single institution.

Post Office RD — Government Guarantee

Post Office deposits, including the 5-year RD, carry a sovereign guarantee from the Government of India. There is no Rs. 5 lakh limit here — the full principal and interest are backed by the central government, making it the safest deposit option available to Indian retail savers.

What About Cooperative Banks and NBFCs?

Deposits with urban cooperative banks are covered by DICGC up to Rs. 5 lakh. State and central cooperative banks similarly have DICGC coverage. However, not all NBFCs accept recurring deposits, and those that do — particularly RD-like chit fund products — do not have DICGC protection. Be extremely cautious with any RD product from a non-bank entity. Verify whether the entity is RBI-registered and DICGC-covered before committing.

Recurring Deposit in 2026 — What Has Changed?

The recurring deposit landscape has evolved meaningfully over the past 12–18 months. Here are the notable developments:

- RBI Monetary Policy Impact: Following a series of repo rate holds and then a 50 basis point cumulative cut in 2025–26, most banks revised their RD rates downward by 15–30 basis points compared to the 2023 peaks. Savvy savers locked in 2023-era rates — a reminder that timing your RD opening matters more than most people realise.

- TDS Threshold Enhancement: The Budget 2025–26 raised the TDS threshold for senior citizens on deposit interest from Rs. 50,000 to Rs. 50,000 (unchanged for regular depositors at Rs. 40,000). While the senior threshold was not raised this year, the proposal remains under active discussion for Budget 2026–27.

- WhatsApp Banking for RD: SBI, HDFC Bank, and ICICI Bank now allow customers to check RD balance, view maturity amount, and receive instalment reminders via their official WhatsApp banking channels — reducing the need to log in to net banking for routine queries.

- Aadhaar-Based Auto-KYC: Opening a new RD at most major banks now requires only an Aadhaar OTP for verification if you already have a savings account — removing the need for physical document submission.

- Green RD Products: Axis Bank and a few other private banks launched ‘green deposit’ variants in 2024-25, where the deposited funds are ring-fenced for ESG-compliant lending. These carry the same interest rate and insurance protection as regular RDs, with a certificate of green deployment issued at maturity.

- Small Finance Bank RD Surge: With SFBs like AU, Ujjivan, and Utkarsh offering rates 75–125 basis points above PSU banks, there has been a visible migration of deposit money to SFBs in the past 18 months. DICGC protection makes this a rational move for the yield-conscious saver.

Expert Tips to Get the Most Out of Your Recurring Deposit

- Rate-lock before the cut: If interest rates are high and you expect the RBI to cut the repo rate, open your RD immediately to lock in the current rate for the full tenure.

- Ladder your RDs: Instead of one large RD, open 3–4 smaller RDs with staggered maturity dates (e.g., one maturing every 6 months). This gives you liquidity flexibility without paying premature closure penalties.

- Submit Form 15G/15H early: Do this at the start of April every financial year. Submitting in November does not prevent TDS deducted from April to October from being deducted.

- Use loan-against-RD in emergencies: If you need funds urgently, borrow against your RD at 1%–2% above your RD rate rather than closing it. You keep the interest clock running and avoid penalty.

- Compare Small Finance Banks: Do not automatically default to your salary bank. Check rates at 2–3 SFBs — a 75 bps difference on Rs. 10,000/month over 3 years translates to roughly Rs. 2,000–3,000 in additional interest.

- Automate for discipline: Set the RD auto-debit date for the day after your salary credit date. This ensures the savings happen before you can spend the money.

- Track in your ITR: Banks send Form 26AS showing TDS deducted. Match this with your interest income in your ITR each year. Errors in 26AS do happen — catching them early avoids tax notices.

13. Frequently Asked Questions — Recurring Deposit

What is the difference between a Recurring Deposit and a Fixed Deposit?

A Fixed Deposit involves depositing a lump sum once, which earns interest until maturity. A Recurring Deposit involves depositing a fixed amount every month over a tenure, with interest calculated on each instalment separately. FD suits those with a lump sum available; RD suits those who want to save gradually from regular income.

Can I open a Recurring Deposit account online?

Yes. All major Indian banks — including SBI, HDFC, ICICI, Axis, and Kotak — allow existing customers to open an RD account entirely online through their net banking portal or mobile app in under 5 minutes. New customers can use Video KYC (V-KYC) to open an account without visiting a branch, a process that is now available at most large banks as of 2026.

Is Recurring Deposit interest taxable in India?

Yes. Interest earned on a Recurring Deposit is fully taxable in India. It is classified as ‘Income from Other Sources’ and added to your total income, then taxed at your applicable slab rate. Banks deduct TDS at 10% if your annual deposit interest exceeds Rs. 40,000 (Rs. 50,000 for seniors). You can submit Form 15G or 15H at the start of the financial year to avoid TDS if your income is below the taxable limit.

What happens if I miss an RD instalment?

Missing an RD instalment attracts a penalty — typically Rs. 1.00 to Rs. 1.50 per Rs. 100 per month of default. The penalty is deducted from the maturity proceeds. If you miss multiple consecutive instalments (usually 3 or more), the bank may allow the RD to lapse or convert it to an irregular account. Reviving an irregular account involves paying all pending instalments with accumulated penalties. Set up an auto-debit mandate to avoid this situation entirely.

Can I take a loan against my Recurring Deposit?

Yes. Most banks allow you to take an overdraft or term loan against your RD account balance, typically up to 80% to 90% of the total deposits made so far. The loan interest rate is usually 1% to 2% above your RD interest rate. This is a better option than premature closure because your RD continues to earn interest while you use the loan amount. The loan is repaid from maturity proceeds.

What is the minimum amount required to open an RD?

The minimum monthly instalment starts at Rs. 100 at State Bank of India and India Post. Most private sector banks like HDFC, ICICI, and Axis require a minimum of Rs. 500 to Rs. 1,000 per month. Small Finance Banks generally require Rs. 500 minimum. There is no upper limit on monthly instalment at most banks.

Is the Post Office Recurring Deposit safer than a bank RD?

Yes, from a sovereign guarantee standpoint. Post Office RD carries the full backing of the Government of India with no upper limit on the guaranteed amount. Bank RDs are protected by DICGC insurance only up to Rs. 5 lakh per depositor per bank. For amounts up to Rs. 5 lakh, both are equally safe. For amounts exceeding Rs. 5 lakh, the Post Office RD has an advantage — though the interest rate at Post Office (currently 6.70%) is generally lower than what competitive banks offer.

Can NRIs open a Recurring Deposit in India?

Yes. NRIs can open NRE RD accounts (interest is tax-free in India, fully repatriable) or NRO RD accounts (interest is taxable in India, limited repatriation up to USD 1 million per year). Most major banks including SBI, HDFC, and ICICI offer NRI RD accounts. The applicable interest rate is the same as for resident Indians on most banks’ rate cards.

What is the maximum tenure for a Recurring Deposit?

For bank RDs, the maximum tenure is typically 10 years. The Post Office RD has a fixed tenure of exactly 5 years, which can be extended in 5-year blocks after maturity. Some banks may offer special long-tenure schemes, but 10 years is the standard maximum.

How is RD different from a SIP?

Both involve regular monthly contributions, but the similarities end there. An RD is a bank deposit that earns fixed, guaranteed interest. A SIP (Systematic Investment Plan) invests your monthly contribution into mutual funds — returns are market-linked, potentially higher over the long term, but not guaranteed. RD is suitable for short-term goals with zero risk tolerance; SIP is suited for long-term goals (7+ years) where you can absorb market ups and downs for higher potential returns.

What is a Flexi RD and how is it different from a regular RD?

A Flexi RD (also called a variable RD) allows you to vary the monthly instalment above the core amount. You commit to a minimum deposit (e.g., Rs. 2,000/month) but can deposit higher amounts (e.g., Rs. 5,000 in a good month) in multiples of a fixed step value. Interest is calculated on each instalment based on the actual amount deposited. This is ideal for irregular income earners who want to save more when they earn more without the rigidity of a fixed monthly commitment.

Can I have multiple RD accounts at the same bank?

Yes. There is no restriction on the number of RD accounts you hold at the same bank or across different banks. Many savers maintain multiple RDs — one for each financial goal (emergency fund, vacation, education, home down payment) — with different tenures and instalment amounts. This goal-based approach makes it easier to track progress and avoids the temptation of merging all savings into one account.

Final Verdict — Is a Recurring Deposit Right for You in 2026?

The Recurring Deposit remains one of the most underrated savings tools for a very specific kind of saver: someone who needs to build savings from regular income, cannot tolerate any capital risk, and wants a fixed, predictable outcome.

It is not the answer for building long-term wealth — for that, equity mutual fund SIPs have a far stronger track record over 7–10 year horizons. But for an emergency fund, a goal due in 1–3 years, or a first savings product for a young earner, an RD is genuinely hard to beat on simplicity, safety, and disciplined execution.

In 2026, the smart approach is to use RDs as the guaranteed, predictable foundation of your savings — and pair them with equity SIPs for longer-term goals. Do not treat the two as competitors; treat them as different tools for different jobs.